Deutsch

Deutsch

Interestingly, when you type into Google “trading signals” the search engine yields 53,600,000 results in 0.33 seconds. In the results section, you will find thousands of sites offering the most diverse opinions and approaches, all labelling themselves as “the best trading signal software solution” while promising astronomically high returns, which an inexperienced and greedy investor might believe.

At ONE-SIGNAL, we pride ourselves on being different and are proud to deliver the best trading signal software to our valued subscribers.

In this article, we will uncover the essence of our uniqueness, from our distinct approach to the fundamental principles and the expertise that fuel our service as a trading signal software provider. At ONE-SIGNAL, we’re dedicated to equipping traders of all levels with the tools they need to navigate the complexities of the financial markets with confidence and precision, thus supporting their trading success.

Our approach as a trading signal software provider

ONE-SIGNAL was developed after numerous years of research on stock market bubbles and the behavior of investors as individuals and in masses. The development of these bubbles is attributed to three psychological factors, being greed, envy, and speculation. Conversely, fear, lack of confidence and disappointment will cause these bubbles to burst.

Based on this, Ara Yalmanian developed ONE-SIGNAL, a non-discretionary system that applies the contrarian investing approach using sentiment indicators. The algorithm systematically analyses market sentiment to recognize emotions associated with bubble formations and predicts subsequent movements.

We believe that sentiment indicators are the best metric to systematically and objectively analyse stock market behavior and predict price movements in every phase of the market. This is based on years of proprietary research and successfully testing our findings in the markets.

What our approach does not include

Within our approach, we do not use:

- Fundamental analysis, so as to avoid valuation inaccuracies

- Technical analysis, so as to avoid self-fulfilling prophecies

- Common indicators, so as to avoid “trend following”

Due to our unique approach, the system pinpoints sentiment trends and follows them until the exaggeration phase, to then change direction strategically. We are the only trading signal software provider to purely rely on sentiment indicators. As a result, we promote a smarter trading technique and more efficient overall trading strategy.

What sets our trading signal software apart

Below, we take a more detailed look at how our approach is realized in our trading signal software functionality, and why this makes our trading signal software the best option for traders.

Efficiency

Despite how complicated a trading system is behind the scenes, the trading signals must be clear, simple and concise and include a risk management system.

That is why our trading signals are short, concise and clear, with an integrated risk management system in the form of a stop loss. Every day, ONE-SIGNAL subscribers receive a LONG or SHORT trading signal, which is valid for one trading day.

That is why our trading signals are short, concise and clear, with an integrated risk management system in the form of a stop loss. Every day, ONE-SIGNAL subscribers receive a LONG or SHORT trading signal, which is valid for one trading day.

With our offering, ONE-SIGNAL Xpert subscribers receive their trading signal 3 hours before the NYSE opening bell. Positions are entered at the NYSE opening bell and closed at the end of the trading day. This enables a systematic approach and allows individuals to establish a trading routine. Traders need only open their trades, go about their daily business, and close the trade at the end of the day.

ONE-SIGNAL Xpress subscribers, on the other hand, receive their trading signals approximately three hours after the NYSE closing bell. If the signal remains unchanged, they can keep their positions overnight. This is geared towards traders who don’t mind having overnight exposure and want to save on transaction costs.

Family-owned and independent

As a family-owned and independent business, at ONE-SIGNAL, we hold a deep-rooted commitment to the success of our subscribers. We understand that our own achievements are intricately tied to the achievements of those we serve. That’s why we go above and beyond to provide unparalleled support and deliver outstanding trading signal software. We pride ourselves on fostering strong and long-lasting relationships, built on trust and mutual success. In short, as a ONE-SIGNAL subscriber, your triumphs are our triumphs, and we are dedicated to working hand-in-hand with you to navigate the complexities of the financial markets and achieve your trading goals.

Trust

ONE-SIGNAL’s distinction lies in its origins as a system developed for personal use. Ara Yalmanian, our Co-Founder, CEO, and System Developer, has relied on ONE-SIGNAL as a trusted trading signal tool for over 10 years. This extensive period of personal utilization has provided us as a trading signal provider with valuable insights and opportunities to refine our trading signal software for reliability. Through continuous, rigorous testing and optimization, ONE-SIGNAL has emerged as a trusted and time-tested trading signal tool to help investors become successful traders by utilizing a proven solution, honed through years of practical experience.

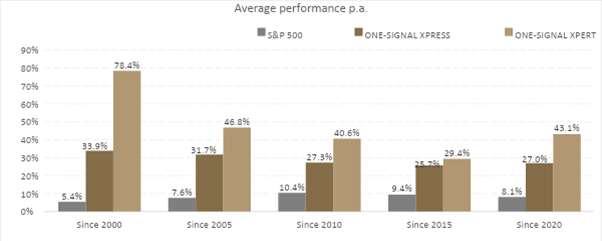

Performance

At ONE-SIGNAL, our track record speaks for itself. As a trusted trading signal software provider, we have consistently outperformed the S&P 500 index since our inception. Since 2000, our performance has surpassed the reference index by an impressive 73%. These remarkable results showcase the effectiveness of our trading signals and the value we bring to our subscribers. Furthermore, in 2022, while the S&P 500 index experienced a significant decline of -19.6%, our offerings stood strong. ONE-SIGNAL Xpress delivered an impressive return of 33.1%, while ONE-SIGNAL Xpert achieved an outstanding return of 68.6%. These exceptional performances demonstrate our commitment to providing the best trading signals and helping our subscribers thrive even in challenging market conditions.

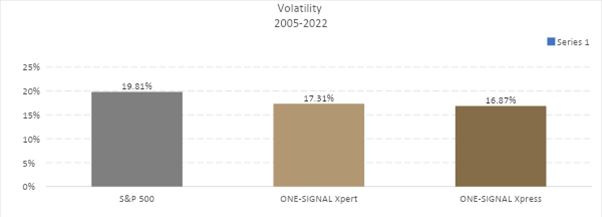

However, in addition to higher returns as shown in the above bar graph , ONE-SIGNAL is also less volatile than the S&P 500 index, which can be noted in the bar chart below.

With the performance and volatility graphs in mind, it’s easy to see how ONE-SIGNAL benefits in every phase of the market, including during periods of higher market volatility. The latter implies falling prices of securities, which our system anticipates and therefore delivers SHORT trading signals for. Long/short investors can choose to follow these, or long-only investors can choose to hedge their portfolios. Additionally, profits are reinvested, creating a compound interest effect.

For inexperienced day traders or time-constraint individuals, we also offer trade execution and money management services, whereby everything, from signal generation to execution, is being taken care of by us, thus encouraging successful trading for investors.

Summary

When it comes to choosing the best trading signal provider, it’s important to consider several factors. Understanding the trading signal provider’s strategy, historic performance, and overall approach is imperative. At ONE-SIGNAL, we offer subscriptions and trade execution services to day traders, focusing on trust, efficiency, and effectiveness.

Our mission in short is to provide investors with an indispensable and proven trading tool that they cannot do without. After years of development and testing, our trading signal software has proven to be reliable and trusted by day traders in their pursuit of success in the financial markets.

With ONE-SIGNAL, you can leverage the power of our trading signal software to assist you in making informed decisions while navigating the complexities of trading with confidence and success. Learn more about the strategy behind our trading signals, or start using our trading signal software with your ONE-SIGNAL to experience ONE-SIGNAL for yourself. Alternatively, if you have any questions, contact our investment experts now.

Disclaimer:

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from our team in ONE-SIGNAL. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request.